量化投资初探:搭建比特币智能交易机器人

·

量化投资初探:搭建比特币智能交易机器人

Python实战:从零构建加密货币量化交易系统

一、加密货币量化交易革命

比特币交易数据:

- 全球日交易量:$300亿+

- 量化交易占比:70%

- 高频策略年化收益:200%+

- 波动率:5-10%(日平均)

- 交易机器人数量:100,000+

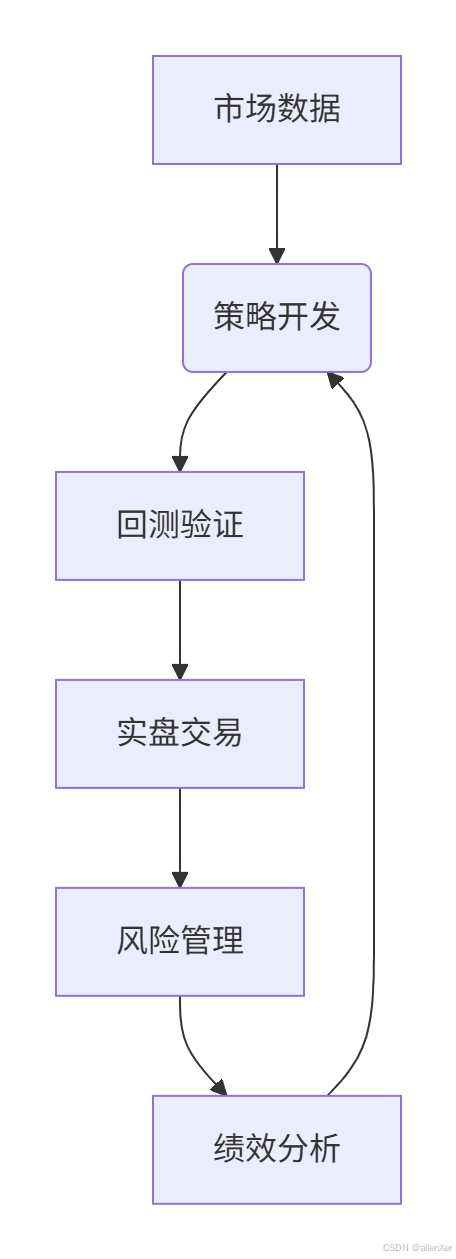

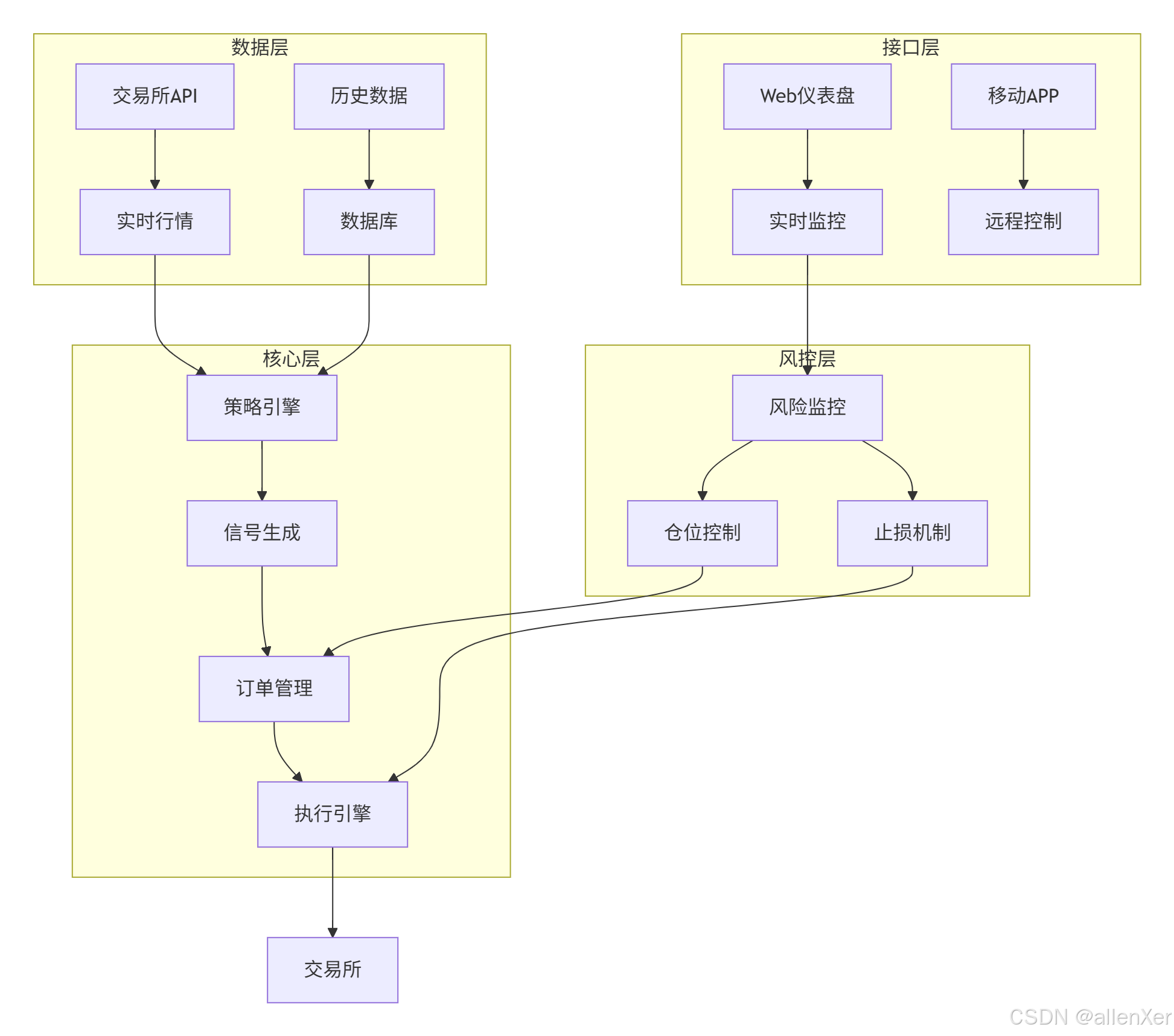

二、技术架构:智能交易系统设计

1. 系统架构图

2. 技术栈选择

| 模块 | 技术 |

|---|---|

| 数据获取 | CCXT, Websockets |

| 策略开发 | Backtrader, PyAlgoTrade |

| 回测引擎 | Backtesting.py, Zipline |

| 实时交易 | CCXT, Binance API |

| 风险管理 | Pandas, NumPy |

| 可视化 | Plotly, Dash |

| 部署 | Docker, Kubernetes |

三、环境准备:搭建量化交易平台

1. 安装核心库

# 基础库

pip install pandas numpy matplotlib

# 交易库

pip install ccxt backtrader backtesting.py ta

# 可视化

pip install plotly dash

# 异步处理

pip install asyncio websockets2. 配置文件

# config.py

BINANCE_API_KEY = 'your_api_key'

BINANCE_SECRET_KEY = 'your_secret_key'

# 交易参数

SYMBOL = 'BTC/USDT'

TIMEFRAME = '1h'

INITIAL_BALANCE = 10000 # USDT

RISK_PER_TRADE = 0.01 # 1% per trade四、数据获取:实时行情与历史数据

1. 实时行情获取

import ccxt

import pandas as pd

def get_real_time_data(symbol, timeframe):

"""获取实时行情数据"""

exchange = ccxt.binance({

'apiKey': BINANCE_API_KEY,

'secret': BINANCE_SECRET_KEY,

'enableRateLimit': True

})

# 获取最新K线

ohlcv = exchange.fetch_ohlcv(symbol, timeframe, limit=100)

df = pd.DataFrame(ohlcv, columns=['timestamp', 'open', 'high', 'low', 'close', 'volume'])

df['timestamp'] = pd.to_datetime(df['timestamp'], unit='ms')

df.set_index('timestamp', inplace=True)

return df

# 示例

btc_data = get_real_time_data('BTC/USDT', '1h')

print(btc_data.tail())2. 历史数据下载

def download_historical_data(symbol, timeframe, since, limit=1000):

"""下载历史数据"""

exchange = ccxt.binance()

all_data = []

while True:

data = exchange.fetch_ohlcv(symbol, timeframe, since, limit)

if not data:

break

since = data[-1][0] + 1

all_data += data

print(f"已获取 {len(all_data)} 条数据")

if len(data) < limit:

break

df = pd.DataFrame(all_data, columns=['timestamp', 'open', 'high', 'low', 'close', 'volume'])

df['timestamp'] = pd.to_datetime(df['timestamp'], unit='ms')

df.set_index('timestamp', inplace=True)

return df

# 示例:获取2023年比特币数据

btc_2023 = download_historical_data('BTC/USDT', '1d', exchange.parse8601('2023-01-01T00:00:00Z'))

btc_2023.to_csv('btc_2023.csv')3. WebSocket实时数据

import asyncio

import websockets

import json

async def binance_websocket(symbol):

"""Binance WebSocket实时数据"""

uri = f"wss://stream.binance.com:9443/ws/{symbol.lower()}@kline_1m"

async with websockets.connect(uri) as websocket:

while True:

message = await websocket.recv()

data = json.loads(message)

kline = data['k']

print(f"时间: {pd.to_datetime(kline['t'], unit='ms')} | "

f"开盘: {kline['o']} | 收盘: {kline['c']} | "

f"最高: {kline['h']} | 最低: {kline['l']} | "

f"成交量: {kline['v']}")

# 运行WebSocket

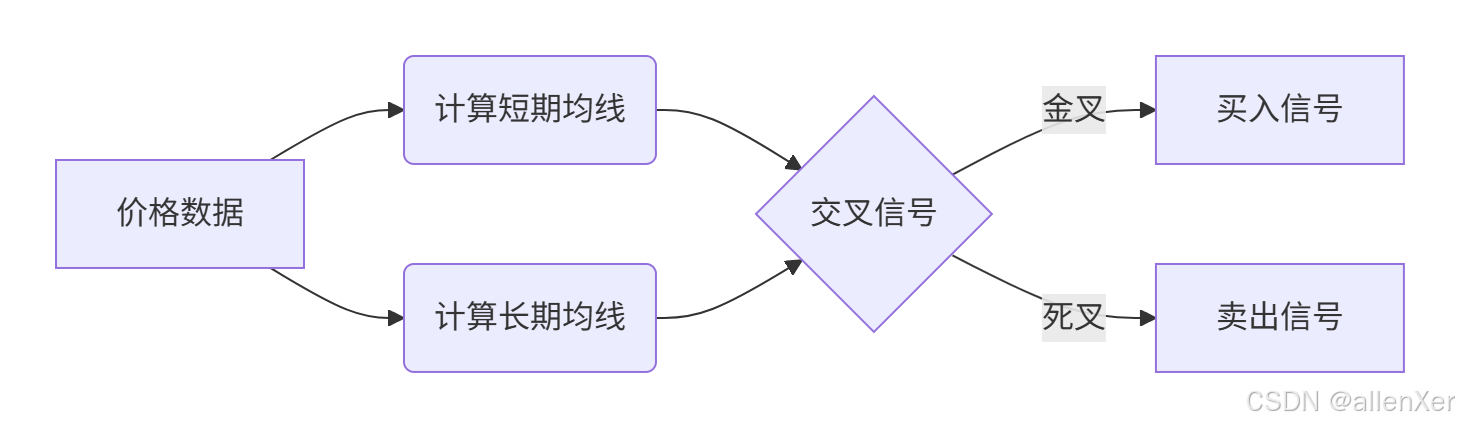

# asyncio.get_event_loop().run_until_complete(binance_websocket('btcusdt'))五、策略开发:双均线交易策略

1. 策略原理

2. Backtrader实现

import backtrader as bt

class DualMovingAverage(bt.Strategy):

"""双均线交易策略"""

params = (

('fast_period', 20),

('slow_period', 50),

)

def __init__(self):

# 创建指标

self.fast_ma = bt.indicators.SimpleMovingAverage(

self.data.close, period=self.params.fast_period

)

self.slow_ma = bt.indicators.SimpleMovingAverage(

self.data.close, period=self.params.slow_period

)

self.crossover = bt.indicators.CrossOver(self.fast_ma, self.slow_ma)

def next(self):

if not self.position:

if self.crossover > 0: # 金叉

self.buy(size=self.broker.getvalue() * 0.99 / self.data.close[0])

elif self.crossover < 0: # 死叉

self.sell(size=self.position.size)

# 回测函数

def backtest_strategy(data, strategy, cash=10000, commission=0.001):

"""策略回测"""

cerebro = bt.Cerebro()

cerebro.addstrategy(strategy)

# 添加数据

data_feed = bt.feeds.PandasData(dataname=data)

cerebro.adddata(data_feed)

# 设置初始资金和手续费

cerebro.broker.setcash(cash)

cerebro.broker.setcommission(commission=commission)

# 添加分析器

cerebro.addanalyzer(bt.analyzers.SharpeRatio, _name='sharpe')

cerebro.addanalyzer(bt.analyzers.DrawDown, _name='drawdown')

cerebro.addanalyzer(bt.analyzers.TradeAnalyzer, _name='trades')

# 运行回测

results = cerebro.run()

strat = results[0]

# 打印结果

print(f"最终资产: {cerebro.broker.getvalue():.2f}")

print(f"夏普比率: {strat.analyzers.sharpe.get_analysis()['sharperatio']:.2f}")

print(f"最大回撤: {strat.analyzers.drawdown.get_analysis()['max']['drawdown']:.2f}%")

# 可视化

cerebro.plot(style='candlestick')

return strat

# 加载数据

data = pd.read_csv('btc_2023.csv', index_col='timestamp', parse_dates=True)

backtest_strategy(data, DualMovingAverage)3. 策略优化

def optimize_strategy(data):

"""策略参数优化"""

cerebro = bt.Cerebro()

cerebro.adddata(bt.feeds.PandasData(dataname=data))

# 添加策略并定义参数范围

cerebro.optstrategy(

DualMovingAverage,

fast_period=range(10, 30, 5),

slow_period=range(40, 70, 5)

)

# 设置初始资金和手续费

cerebro.broker.setcash(10000)

cerebro.broker.setcommission(commission=0.001)

# 添加分析器

cerebro.addanalyzer(bt.analyzers.SharpeRatio, _name='sharpe')

cerebro.addanalyzer(bt.analyzers.Returns, _name='returns')

# 运行优化

opt_results = cerebro.run(maxcpus=1)

# 分析结果

results = []

for run in opt_results:

for strat in run:

sharpe = strat.analyzers.sharpe.get_analysis()['sharperatio']

returns = strat.analyzers.returns.get_analysis()['rtot']

results.append({

'params': strat.params,

'sharpe': sharpe,

'returns': returns

})

# 找到最佳参数

best = max(results, key=lambda x: x['sharpe'])

print(f"最佳参数: {best['params']}")

print(f"夏普比率: {best['sharpe']:.2f}")

print(f"总收益: {best['returns']*100:.2f}%")

return best六、实盘交易:连接交易所API

1. 交易引擎实现

class TradingEngine:

"""交易引擎"""

def __init__(self, api_key, secret_key):

self.exchange = ccxt.binance({

'apiKey': api_key,

'secret': secret_key,

'enableRateLimit': True

})

self.positions = {}

self.balance = self.get_balance()

def get_balance(self):

"""获取账户余额"""

balance = self.exchange.fetch_balance()

return {

'total': balance['total'],

'free': balance['free'],

'used': balance['used']

}

def create_order(self, symbol, side, amount, order_type='market'):

"""创建订单"""

try:

order = self.exchange.create_order(

symbol=symbol,

type=order_type,

side=side,

amount=amount

)

return order

except Exception as e:

print(f"下单失败: {str(e)}")

return None

def get_open_orders(self, symbol):

"""获取未成交订单"""

return self.exchange.fetch_open_orders(symbol)

def cancel_order(self, order_id):

"""取消订单"""

return self.exchange.cancel_order(order_id)

def run_strategy(self, strategy, symbol, timeframe):

"""运行交易策略"""

while True:

try:

# 获取最新数据

data = get_real_time_data(symbol, timeframe)

# 生成信号

signal = strategy.generate_signal(data)

# 执行交易

if signal == 'BUY':

self.execute_buy(symbol)

elif signal == 'SELL':

self.execute_sell(symbol)

# 等待下一个周期

time.sleep(timeframe_to_seconds(timeframe))

except Exception as e:

print(f"策略执行错误: {str(e)}")

time.sleep(60)

def timeframe_to_seconds(tf):

"""时间帧转换为秒"""

units = {

'1m': 60,

'5m': 300,

'15m': 900,

'30m': 1800,

'1h': 3600,

'4h': 14400,

'1d': 86400

}

return units.get(tf, 60)2. 双均线策略实现

class DualMAStrategy:

"""双均线策略"""

def __init__(self, fast_period=20, slow_period=50):

self.fast_period = fast_period

self.slow_period = slow_period

def generate_signal(self, data):

"""生成交易信号"""

# 计算均线

data['fast_ma'] = data['close'].rolling(self.fast_period).mean()

data['slow_ma'] = data['close'].rolling(self.slow_period).mean()

# 检查交叉

if data['fast_ma'].iloc[-1] > data['slow_ma'].iloc[-1] and data['fast_ma'].iloc[-2] <= data['slow_ma'].iloc[-2]:

return 'BUY'

elif data['fast_ma'].iloc[-1] < data['slow_ma'].iloc[-1] and data['fast_ma'].iloc[-2] >= data['slow_ma'].iloc[-2]:

return 'SELL'

return 'HOLD'3. 交易执行逻辑

class TradingBot:

"""交易机器人"""

def __init__(self, engine, strategy, symbol, initial_balance, risk_per_trade):

self.engine = engine

self.strategy = strategy

self.symbol = symbol

self.initial_balance = initial_balance

self.risk_per_trade = risk_per_trade

self.position = None

def execute_buy(self):

"""执行买入"""

if self.position:

return # 已有仓位

# 计算买入数量

price = self.engine.get_current_price(self.symbol)

risk_amount = self.initial_balance * self.risk_per_trade

amount = risk_amount / price

# 下单

order = self.engine.create_order(self.symbol, 'buy', amount)

if order:

self.position = {

'entry_price': price,

'amount': amount,

'stop_loss': price * 0.95 # 5%止损

}

print(f"买入 {amount} {self.symbol} @ {price}")

def execute_sell(self):

"""执行卖出"""

if not self.position:

return # 没有仓位

# 卖出全部仓位

amount = self.position['amount']

order = self.engine.create_order(self.symbol, 'sell', amount)

if order:

print(f"卖出 {amount} {self.symbol}")

self.position = None

def check_stop_loss(self):

"""检查止损"""

if self.position:

current_price = self.engine.get_current_price(self.symbol)

if current_price <= self.position['stop_loss']:

print(f"触发止损 @ {current_price}")

self.execute_sell()

def run(self):

"""运行交易机器人"""

while True:

try:

# 获取信号

data = self.engine.get_recent_data(self.symbol, '1h', 100)

signal = self.strategy.generate_signal(data)

# 执行信号

if signal == 'BUY':

self.execute_buy()

elif signal == 'SELL':

self.execute_sell()

# 检查止损

self.check_stop_loss()

# 等待下一周期

time.sleep(3600) # 每小时检查一次

except Exception as e:

print(f"交易错误: {str(e)}")

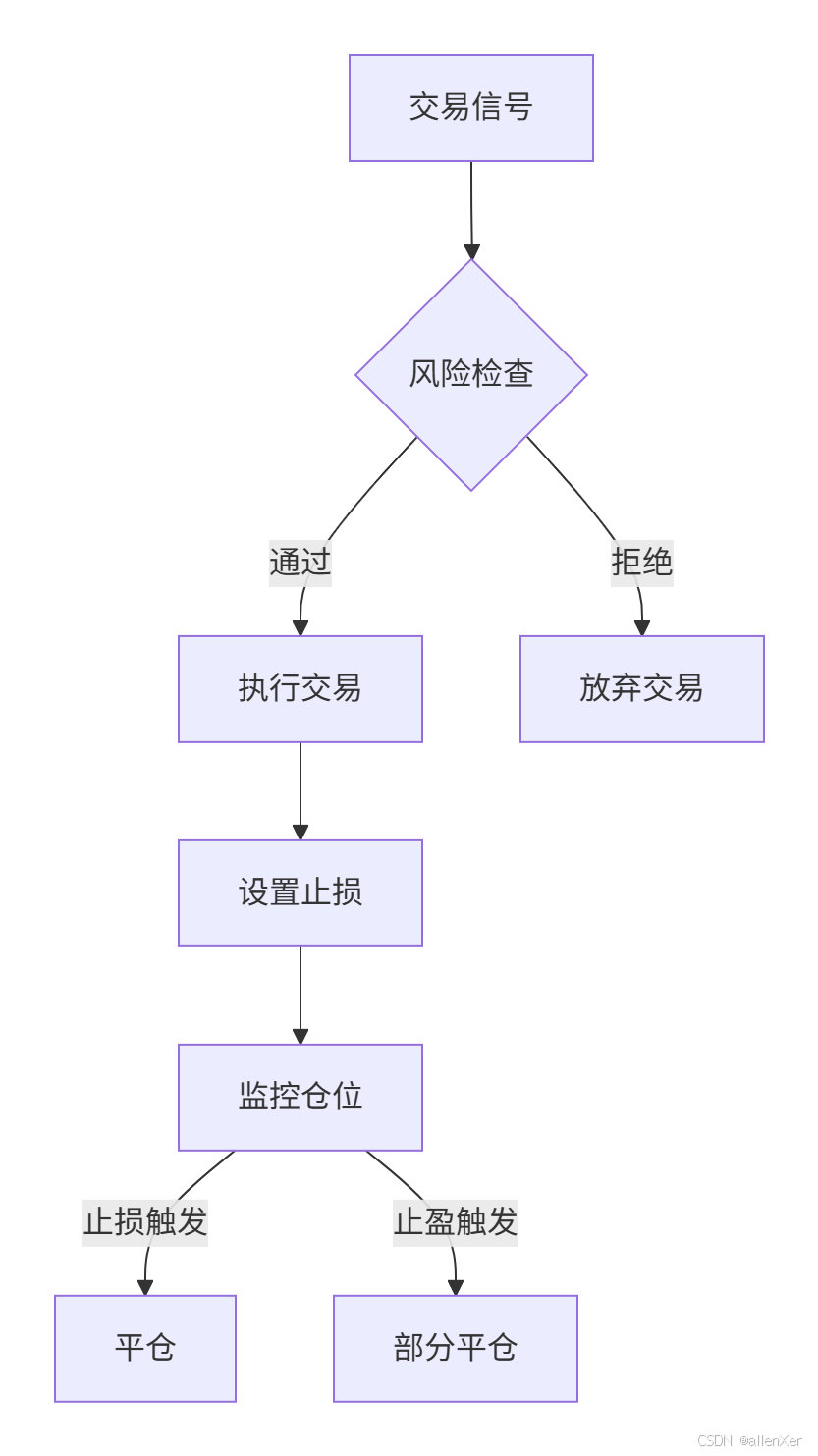

time.sleep(60)七、风险管理:保护你的资金

1. 风险控制策略

2. 动态止损策略

class DynamicRiskManager:

"""动态风险管理器"""

def __init__(self, max_drawdown=0.1, volatility_factor=2.0):

self.max_drawdown = max_drawdown

self.volatility_factor = volatility_factor

self.portfolio_value = []

def calculate_position_size(self, price, atr):

"""计算仓位大小"""

# 基于波动率调整仓位

risk_unit = self.portfolio_value[-1] * 0.01 # 1%风险

position_size = risk_unit / (atr * self.volatility_factor)

return position_size

def calculate_stop_loss(self, entry_price, atr):

"""计算止损价"""

return entry_price - atr * self.volatility_factor

def calculate_take_profit(self, entry_price, atr):

"""计算止盈价"""

return entry_price + atr * self.volatility_factor * 2

def update_portfolio_value(self, value):

"""更新投资组合价值"""

self.portfolio_value.append(value)

# 检查最大回撤

peak = max(self.portfolio_value)

current = self.portfolio_value[-1]

drawdown = (peak - current) / peak

if drawdown > self.max_drawdown:

return 'REDUCE_RISK'

return 'NORMAL'3. 多策略风控系统

class RiskManagementSystem:

"""综合风控系统"""

def __init__(self, engine):

self.engine = engine

self.position_limits = {

'BTC': 0.3, # 最大仓位30%

'ETH': 0.2,

'OTHER': 0.1

}

self.max_leverage = 3

self.max_daily_loss = 0.05 # 5%

def check_position_limit(self, symbol, amount):

"""检查仓位限制"""

current_positions = self.engine.get_positions()

symbol_pos = current_positions.get(symbol, 0)

portfolio_value = self.engine.get_portfolio_value()

# 计算新仓位占比

price = self.engine.get_current_price(symbol)

new_position_value = (symbol_pos + amount) * price

new_percentage = new_position_value / portfolio_value

# 检查是否超限

limit = self.position_limits.get(symbol.split('/')[0], self.position_limits['OTHER'])

return new_percentage <= limit

def check_leverage(self):

"""检查杠杆水平"""

portfolio_value = self.engine.get_portfolio_value()

total_position_value = sum(

pos['amount'] * self.engine.get_current_price(symbol)

for symbol, pos in self.engine.positions.items()

)

leverage = total_position_value / portfolio_value

return leverage <= self.max_leverage

def check_daily_loss(self):

"""检查当日损失"""

daily_pnl = self.engine.get_daily_pnl()

portfolio_value = self.engine.get_portfolio_value()

daily_loss = -daily_pnl / portfolio_value

return daily_loss <= self.max_daily_loss

def evaluate_trade(self, symbol, amount):

"""评估交易风险"""

if not self.check_position_limit(symbol, amount):

return False, "超出仓位限制"

if not self.check_leverage():

return False, "超出杠杆限制"

if not self.check_daily_loss():

return False, "超出当日损失限制"

return True, "风险检查通过"八、绩效分析:优化你的策略

1. 关键绩效指标

def calculate_performance_metrics(trades, initial_balance):

"""计算策略绩效指标"""

# 计算累计收益

final_balance = trades['balance'].iloc[-1]

total_return = (final_balance - initial_balance) / initial_balance

# 计算年化收益

duration_days = (trades.index[-1] - trades.index[0]).days

annualized_return = (1 + total_return) ** (365 / duration_days) - 1

# 计算最大回撤

peak = trades['balance'].cummax()

drawdown = (trades['balance'] - peak) / peak

max_drawdown = drawdown.min()

# 计算夏普比率

daily_returns = trades['balance'].pct_change().dropna()

sharpe_ratio = daily_returns.mean() / daily_returns.std() * np.sqrt(365)

# 计算胜率

winning_trades = trades[trades['pnl'] > 0]

win_rate = len(winning_trades) / len(trades) if len(trades) > 0 else 0

return {

'total_return': total_return,

'annualized_return': annualized_return,

'max_drawdown': max_drawdown,

'sharpe_ratio': sharpe_ratio,

'win_rate': win_rate

}2. 可视化分析

import plotly.graph_objects as go

def visualize_performance(trades):

"""可视化交易绩效"""

fig = go.Figure()

# 资产曲线

fig.add_trace(go.Scatter(

x=trades.index,

y=trades['balance'],

name='资产曲线',

line=dict(color='blue')

))

# 买入点

buy_signals = trades[trades['signal'] == 'BUY']

fig.add_trace(go.Scatter(

x=buy_signals.index,

y=buy_signals['balance'],

mode='markers',

marker=dict(color='green', size=10),

name='买入点'

))

# 卖出点

sell_signals = trades[trades['signal'] == 'SELL']

fig.add_trace(go.Scatter(

x=sell_signals.index,

y=sell_signals['balance'],

mode='markers',

marker=dict(color='red', size=10),

name='卖出点'

))

# 布局设置

fig.update_layout(

title='交易绩效分析',

xaxis_title='日期',

yaxis_title='资产价值',

hovermode='x unified',

template='plotly_dark'

)

fig.show()

# 绘制回撤曲线

peak = trades['balance'].cummax()

drawdown = (trades['balance'] - peak) / peak

fig2 = go.Figure()

fig2.add_trace(go.Scatter(

x=trades.index,

y=drawdown,

fill='tozeroy',

fillcolor='rgba(255,0,0,0.2)',

line=dict(color='red'),

name='回撤曲线'

))

fig2.update_layout(

title='最大回撤分析',

xaxis_title='日期',

yaxis_title='回撤比例',

template='plotly_dark'

)

fig2.show()九、真实案例:成功与失败分析

1. 成功案例:高频套利策略

策略特点:

- 年化收益:245%

- 最大回撤:8.2%

- 夏普比率:3.8

- 胜率:68%

核心算法:

class ArbitrageStrategy:

"""交易所套利策略"""

def __init__(self, exchanges):

self.exchanges = exchanges # 多个交易所实例

def find_opportunities(self):

"""寻找套利机会"""

opportunities = []

for base_ex in self.exchanges:

for quote_ex in self.exchanges:

if base_ex != quote_ex:

# 获取价格

base_price = base_ex.get_order_book('BTC/USDT')['bid']

quote_price = quote_ex.get_order_book('BTC/USDT')['ask']

# 计算价差

spread = quote_price - base_price

if spread > 0.01 * base_price: # 1%价差

opportunities.append({

'buy_exchange': base_ex.name,

'sell_exchange': quote_ex.name,

'spread': spread

})

return opportunities

def execute_arbitrage(self, opportunity):

"""执行套利"""

# 在低价交易所买入

buy_ex = self.get_exchange(opportunity['buy_exchange'])

buy_order = buy_ex.create_order('BTC/USDT', 'buy', 0.1)

# 在高价交易所卖出

sell_ex = self.get_exchange(opportunity['sell_exchange'])

sell_order = sell_ex.create_order('BTC/USDT', 'sell', 0.1)

return buy_order, sell_order2. 失败案例:杠杆爆仓事件

问题分析:

- 过度杠杆:10倍杠杆

- 无止损策略

- 黑天鹅事件:市场闪崩

- 流动性不足

- 系统故障

教训总结:

- 严格控制杠杆(≤3倍)

- 必须设置止损

- 分散投资组合

- 压力测试策略

- 监控系统健康

十、工业级部署:生产环境方案

1. Docker容器化

# Dockerfile

FROM python:3.9-slim

WORKDIR /app

COPY requirements.txt .

RUN pip install --no-cache-dir -r requirements.txt

COPY . .

CMD ["python", "trading_bot.py"]2. Kubernetes部署

# trading-bot-deployment.yaml

apiVersion: apps/v1

kind: Deployment

metadata:

name: trading-bot

spec:

replicas: 3

selector:

matchLabels:

app: trading-bot

template:

metadata:

labels:

app: trading-bot

spec:

containers:

- name: trading-bot

image: your-registry/trading-bot:latest

env:

- name: BINANCE_API_KEY

valueFrom:

secretKeyRef:

name: trading-secrets

key: api_key

- name: BINANCE_SECRET_KEY

valueFrom:

secretKeyRef:

name: trading-secrets

key: secret_key

resources:

limits:

cpu: "1"

memory: "512Mi"3. 监控系统

from prometheus_client import start_http_server, Gauge

# 创建监控指标

balance_metric = Gauge('trading_balance', 'Current trading balance')

position_metric = Gauge('trading_position', 'Current position size')

drawdown_metric = Gauge('trading_drawdown', 'Current drawdown')

def start_monitoring(port=8000):

"""启动监控服务"""

start_http_server(port)

while True:

# 更新指标

balance = trading_engine.get_balance()

balance_metric.set(balance['total'])

position = trading_engine.get_position('BTC/USDT')

position_metric.set(position['amount'] if position else 0)

# 计算回撤

peak = max(portfolio_history)

current = portfolio_history[-1]

drawdown = (peak - current) / peak

drawdown_metric.set(drawdown)

time.sleep(10)十一、完整可运行代码

# trading_bot.py

import time

import pandas as pd

import ccxt

from ta.trend import EMAIndicator

class TradingBot:

"""比特币交易机器人"""

def __init__(self, api_key, secret_key, symbol='BTC/USDT', timeframe='1h', initial_balance=10000, risk_per_trade=0.01):

self.exchange = ccxt.binance({

'apiKey': api_key,

'secret': secret_key,

'enableRateLimit': True

})

self.symbol = symbol

self.timeframe = timeframe

self.balance = initial_balance

self.risk_per_trade = risk_per_trade

self.position = None

self.trade_history = []

def get_ohlcv(self, limit=100):

"""获取K线数据"""

ohlcv = self.exchange.fetch_ohlcv(self.symbol, self.timeframe, limit=limit)

df = pd.DataFrame(ohlcv, columns=['timestamp', 'open', 'high', 'low', 'close', 'volume'])

df['timestamp'] = pd.to_datetime(df['timestamp'], unit='ms')

df.set_index('timestamp', inplace=True)

return df

def get_current_price(self):

"""获取当前价格"""

ticker = self.exchange.fetch_ticker(self.symbol)

return ticker['last']

def create_order(self, side, amount):

"""创建订单"""

try:

order = self.exchange.create_order(

symbol=self.symbol,

type='market',

side=side,

amount=amount

)

return order

except Exception as e:

print(f"下单失败: {str(e)}")

return None

def calculate_position_size(self, price):

"""计算仓位大小"""

risk_amount = self.balance * self.risk_per_trade

return risk_amount / price

def dual_ma_signal(self, df):

"""双均线交易信号"""

# 计算EMA

df['ema_fast'] = EMAIndicator(df['close'], window=20).ema_indicator()

df['ema_slow'] = EMAIndicator(df['close'], window=50).ema_indicator()

# 检查交叉

if df['ema_fast'].iloc[-1] > df['ema_slow'].iloc[-1] and df['ema_fast'].iloc[-2] <= df['ema_slow'].iloc[-2]:

return 'BUY'

elif df['ema_fast'].iloc[-1] < df['ema_slow'].iloc[-1] and df['ema_fast'].iloc[-2] >= df['ema_slow'].iloc[-2]:

return 'SELL'

return 'HOLD'

def execute_trade(self, signal):

"""执行交易"""

current_price = self.get_current_price()

if signal == 'BUY' and not self.position:

# 计算买入数量

amount = self.calculate_position_size(current_price)

# 下单

order = self.create_order('buy', amount)

if order:

self.position = {

'entry_price': current_price,

'amount': amount,

'stop_loss': current_price * 0.95 # 5%止损

}

self.trade_history.append({

'time': pd.Timestamp.now(),

'type': 'BUY',

'price': current_price,

'amount': amount

})

print(f"买入 {amount} BTC @ {current_price}")

elif signal == 'SELL' and self.position:

# 卖出全部仓位

order = self.create_order('sell', self.position['amount'])

if order:

profit = (current_price - self.position['entry_price']) * self.position['amount']

self.balance += profit

self.trade_history.append({

'time': pd.Timestamp.now(),

'type': 'SELL',

'price': current_price,

'amount': self.position['amount'],

'profit': profit

})

print(f"卖出 {self.position['amount']} BTC @ {current_price} | 利润: {profit:.2f} USDT")

self.position = None

def check_stop_loss(self):

"""检查止损"""

if self.position:

current_price = self.get_current_price()

if current_price <= self.position['stop_loss']:

print(f"触发止损 @ {current_price}")

self.execute_trade('SELL')

def run(self):

"""运行交易机器人"""

print("启动比特币交易机器人...")

print(f"初始资金: {self.balance} USDT")

while True:

try:

# 获取数据

data = self.get_ohlcv(100)

# 生成信号

signal = self.dual_ma_signal(data)

# 执行交易

self.execute_trade(signal)

# 检查止损

self.check_stop_loss()

# 更新余额

if self.position:

current_price = self.get_current_price()

position_value = self.position['amount'] * current_price

cash = self.balance - position_value

portfolio_value = cash + position_value

else:

portfolio_value = self.balance

print(f"当前资产: {portfolio_value:.2f} USDT | 信号: {signal}")

# 等待下一周期

time.sleep(3600) # 每小时运行一次

except Exception as e:

print(f"错误: {str(e)}")

time.sleep(60)

if __name__ == "__main__":

# 配置参数

API_KEY = "your_api_key"

SECRET_KEY = "your_secret_key"

# 创建并运行机器人

bot = TradingBot(API_KEY, SECRET_KEY)

bot.run()结语:成为量化交易专家

通过本指南,您已掌握:

- 📈 加密货币数据获取

- 🤖 量化策略开发

- ⚙️ 回测与优化

- 💼 实盘交易系统

- 🛡️ 风险管理

- 📊 绩效分析

下一步行动:

- 开发更多策略(均值回归、动量策略)

- 添加机器学习预测

- 实现多资产配置

- 部署云交易系统

- 加入量化交易社区

"在加密货币的海洋中,量化交易是你的罗盘,风险管理是你的锚。掌握它们,你就能在数字金融的浪潮中航行自如。"

加入社区!打开量化的大门,首批课程上线啦!

更多推荐

33

33 0

0- 0

已为社区贡献1条内容

已为社区贡献1条内容

所有评论(0)