量化交易 - 概念板块+基本面选股【miniQmt+joinQuant】

哎,选股这块还是转战 joinQuant吧 (但是joinQuant的板块比较差,没有概念板块, 所以需要与qmt结合起来)这一步,可以根据个人喜好来筛选, 你可以根据上涨幅度、是否涨停等来筛选。可以发现, 价格是可以获取的, 但pe值全为0!但却下载不了数据, 一直等待中, 排查了半天。可以看我GitHub上对应项目。用qmt获取不到pe市盈率。我这里以基本面作为筛选., 一下子就正常使用了。

·

一、下载 保存板块到本地

from xtquant import xtdata

# 1. 下载最新板块分类信息(建议初始化时调用)

xtdata.download_sector_data()

# 2. 获取所有板块名称

sectors = xtdata.get_sector_list()

path = 'data/qmt_概念板块.txt'

save_to_local = True

if save_to_local:

with open(path, 'w', encoding='utf-8') as f:

f.write('\n'.join(sectors))

保存后如下图:

二、根据板块名称获取股票列表

from xtquant import xtdata

stocks = xtdata.get_stock_list_in_sector('GNAI算力芯片')

print(stocks)结果如下:

三、下载财务数据【易踩坑】

官方:股票数据 | 迅投知识库

官方用的是这个函数:

xtdata.download_financial_data(["000001.SZ"], table_list=["Balance","Income"])

但却下载不了数据, 一直等待中, 排查了半天

后面换了一个函数xtdata.download_financial_data2, 一下子就正常使用了

from xtquant import xtdata

# 取数据前请确保已下载所需要的财务数据

xtdata.download_financial_data2(["000001.SZ"], table_list=["Balance","Income"])

print('finish download.')

x = xtdata.get_financial_data(["000001.SZ"],["Balance","Income"])

print(x)

结果如下:

finish download.

{'000001.SZ': {'Balance': m_timetag m_anntime internal_shoule_recv ... m_petainedProfit m_provisionTransactionRisk m_otherReserves

0 19911231 19920430 NaN ... NaN NaN NaN

1 19921231 19930226 NaN ... NaN NaN NaN

2 19931231 19940329 NaN ... NaN NaN NaN

3 19940630 19940630 NaN ... NaN NaN NaN

4 19941231 19950127 NaN ... NaN NaN NaN

.. ... ... ... ... ... ... ...

104 20230630 20230824 NaN ... NaN NaN NaN

105 20230930 20231025 NaN ... NaN NaN NaN

106 20231231 20240315 NaN ... NaN NaN NaN

107 20240331 20240420 NaN ... NaN NaN NaN

108 20250331 20250419 NaN ... NaN NaN NaN

[109 rows x 160 columns], 'Income': m_timetag m_anntime revenue_inc earned_premium ... tot_compreh_inc_parent_comp actual_ann_dt operating_revenue cost_of_goods_sold

0 19911231 19920430 3.346900e+08 0.0 ... 0.0 0.0 0.0 0.0

1 19921231 19930226 4.755108e+08 0.0 ... 0.0 0.0 0.0 0.0

2 19930630 19930805 2.664955e+08 0.0 ... 0.0 0.0 0.0 0.0

3 19931231 19940329 NaN 0.0 ... 0.0 0.0 0.0 0.0

4 19940630 19940630 NaN 0.0 ... 0.0 0.0 0.0 0.0

.. ... ... ... ... ... ... ... ... ...

144 20230630 20230824 8.861000e+10 NaN ... 0.0 0.0 0.0 0.0

145 20230930 20231025 1.276340e+11 NaN ... 0.0 0.0 0.0 0.0

146 20231231 20240315 1.646990e+11 NaN ... 0.0 0.0 0.0 0.0

147 20240331 20240420 3.877000e+10 NaN ... 0.0 0.0 0.0 0.0

148 20250331 20250419 3.370900e+10 NaN ... 0.0 0.0 0.0 0.0

[149 rows x 84 columns]}}其他数据, 如果你想下载,可以用这样:

from xtquant import xtdata

import pandas as pd

codes = ["000001.SZ", "600519.SH"] # 替换成你的股票代码

for code in codes:

xtdata.download_history_data(code, start_time='20250801',period='1d')

x = xtdata.get_market_data(["open", "close"], codes, count=3)

print(x)结果如下:

{'open': 20250815 20250818 20250819

000001.SZ 12.23 12.06 12.1

600519.SH 1426.01 1426.99 1433.5, 'close': 20250815 20250818 20250819

000001.SZ 12.08 12.08 12.05

600519.SH 1422.08 1428.50 1439.60}这里又有一个坑!

用qmt获取不到pe市盈率

代码如下:

from xtquant import xtdata

codes = ["000001.SZ", "600519.SH", "003010.SZ"] # 替换成你的股票代码

for code in codes:

# xtdata.download_history_data(code, start_time='20250801',period='1d')

xtdata.download_history_data(code, start_time='20250818',period='tick')

x = xtdata.get_market_data_ex(['lastPrice', 'pe'], codes, period='tick', count=3)

print(x)

结果如下:

{'000001.SZ': lastPrice pe

20250819112954 12.04 0.0

20250819112957 12.05 0.0

20250819113000 12.05 0.0, '003010.SZ': lastPrice pe

20250819112954 53.70 0.0

20250819112957 53.71 0.0

20250819113000 53.71 0.0, '600519.SH': lastPrice pe

20250819112954 1439.66 0.0

20250819112958 1439.66 0.0

20250819113000 1439.60 0.0}可以发现, 价格是可以获取的, 但pe值全为0!

哎,选股这块还是转战 joinQuant吧 (但是joinQuant的板块比较差,没有概念板块, 所以需要与qmt结合起来)

四、根据基本面来筛选股票

这一步,可以根据个人喜好来筛选, 你可以根据上涨幅度、是否涨停等来筛选

我这里以基本面作为筛选.

筛选标准

最近5年roe均大于当年的平均水平, 最近一年roe排名前30%, 按照板块+roe降序排序

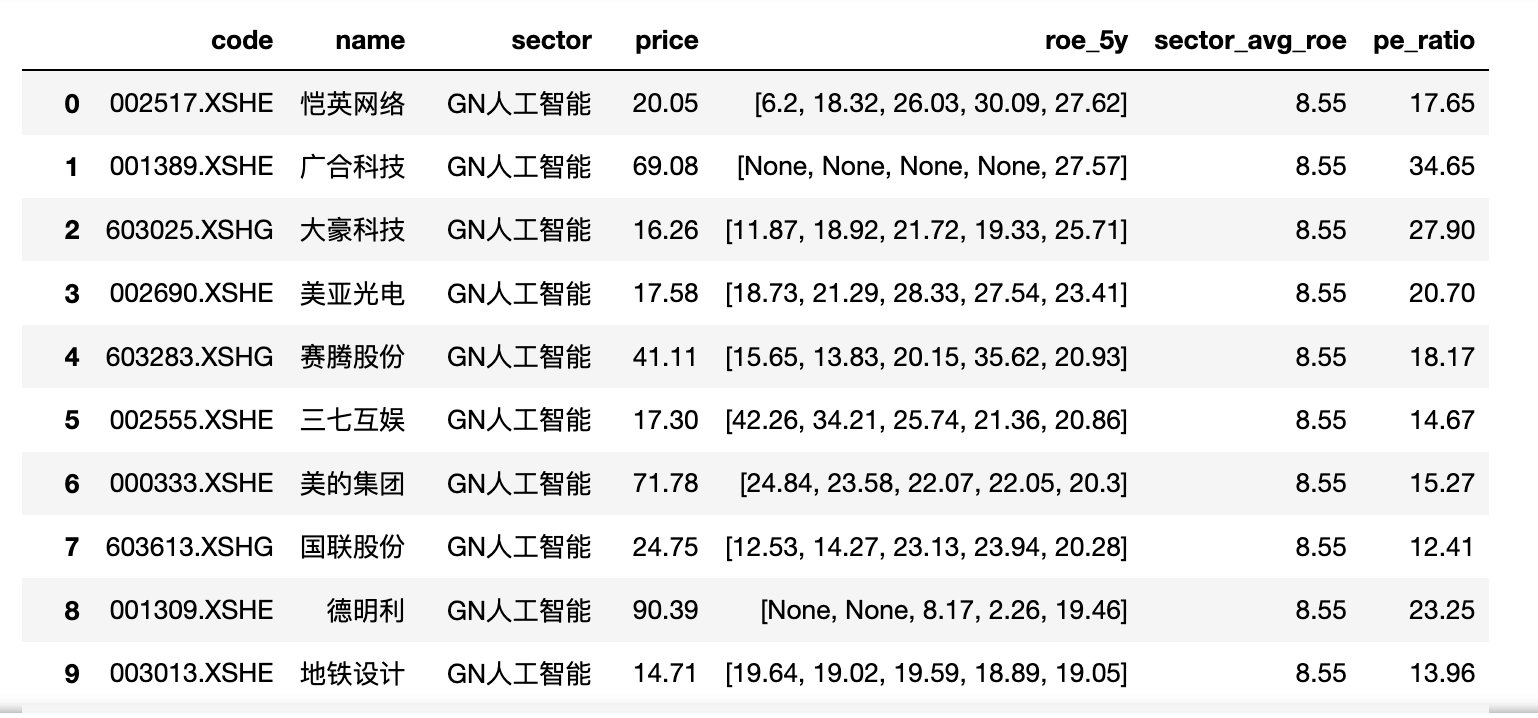

输出: 股票代码,股票名,板块名, 股价, 最近5年的roe, 板块平均roe, 市盈率

代码:

# qmt_概念板块.json 可以在https://github.com/JizhiXiang/Quant-Strategy 对应的QQ群里下载资源

# ====== 第1部分:读取数据与筛板块 ======

import json, pandas as pd

from jqdata import *

from datetime import datetime

with open('qmt_概念板块.json', 'r', encoding='utf-8') as f:

sectors = json.load(f)

keyword = "人工智能" #人形机器人

result = {k: v for k, v in sectors.items() if keyword in k}

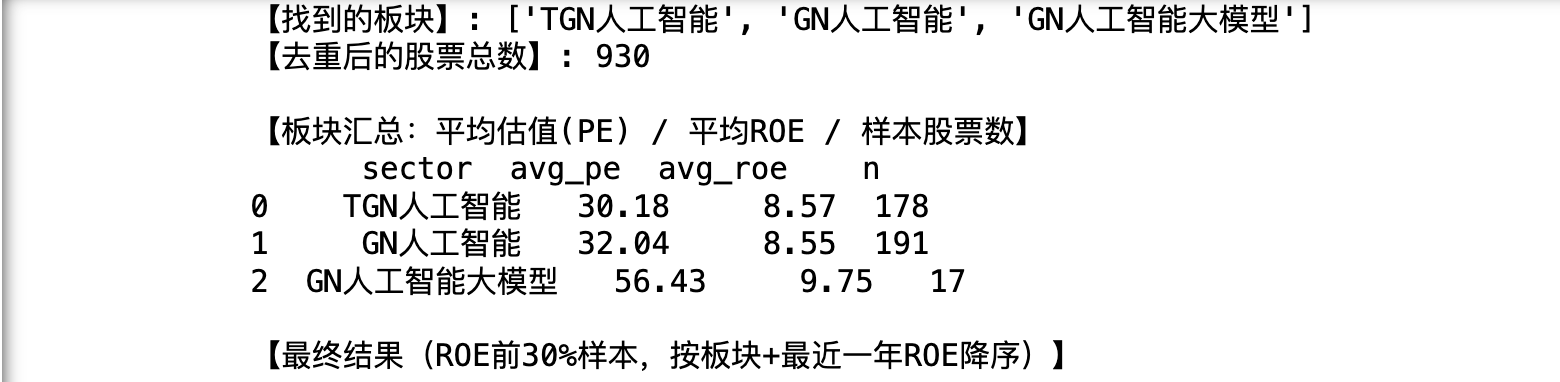

print("【找到的板块】:", list(result.keys()))

print("【去重后的股票总数】:", len({c for v in result.values() for c in v}))

def to_jq_code(c):

return c.replace('.SH','.XSHG').replace('.SZ','.XSHE')

stocks = sorted({

to_jq_code(c) for v in result.values() for c in v

if c.startswith(('60','00'))

})

# ====== 第2部分:获取最近5年财务数据并过滤 ======

y0 = datetime.today().year

years = list(range(y0-5, y0)) # y0-5 到 y0-1

q = query(valuation.code, valuation.pe_ratio, indicator.roe).filter(valuation.code.in_(stocks))

df = pd.concat([get_fundamentals(q, statDate=y).assign(year=y) for y in years], ignore_index=True)

# 当年样本平均ROE,并标记是否大于平均

df['roe_avg_year'] = df.groupby('year')['roe'].transform('mean')

df['gt_avg'] = df['roe'] > df['roe_avg_year']

# 条件:最近5年ROE均大于当年平均

flag_5y = df.groupby('code')['gt_avg'].all()

df = df[df.code.isin(flag_5y[flag_5y].index)].copy()

# 最近一年(用于排名与板块均值)

last = df[df.year == y0-1].copy()

# ====== 第3部分:多对多映射并“拆行” ======

rel_rows = []

for sec_name, codes in result.items():

for c in codes:

if c.startswith(('60','00')):

rel_rows.append((to_jq_code(c), sec_name))

rel = pd.DataFrame(rel_rows, columns=['code', 'sector']).drop_duplicates()

# 将 last 拆成每行一个板块

last_exploded = last.merge(rel, on='code', how='inner')

# 板块平均ROE/PE(最近一年),兼容旧版 pandas 的写法

sector_summary = (last_exploded.groupby('sector')

.agg({'pe_ratio':'mean','roe':'mean','code':pd.Series.nunique})

.reset_index()

.rename(columns={'pe_ratio':'avg_pe','roe':'avg_roe','code':'n'}))

# 映射到明细

sector_avg_roe_map = dict(zip(sector_summary['sector'], sector_summary['avg_roe']))

sector_avg_pe_map = dict(zip(sector_summary['sector'], sector_summary['avg_pe']))

last_exploded['sector_avg_roe'] = last_exploded['sector'].map(sector_avg_roe_map)

last_exploded['sector_avg_pe'] = last_exploded['sector'].map(sector_avg_pe_map)

# ====== 第4部分:取最近一年ROE前30%(按股票,不按板块行) ======

cut = last['roe'].quantile(0.7)

top_codes = set(last[last['roe'] >= cut]['code'])

res = last_exploded[last_exploded['code'].isin(top_codes)].copy()

# ====== 第5部分:补充“最近5年ROE列表”、名称与现价 ======

roe_hist = (df.pivot_table(index='code', columns='year', values='roe')

.reindex(columns=years))

def _to_list(s):

vals = []

for x in s.values:

if pd.isna(x):

vals.append(None)

else:

vals.append(round(float(x), 4))

return vals

roe_hist_list = roe_hist.apply(_to_list, axis=1).to_dict()

res['roe_5y'] = res['code'].map(roe_hist_list)

names = get_all_securities(['stock']).display_name.to_dict()

res['name'] = res['code'].map(names)

res['price'] = res['code'].apply(

lambda x: float(get_price(x, count=1, end_date=datetime.today()).close[0])

)

# ====== 第6部分:分部分输出 ======

# 6.1 板块层面汇总(平均估值、平均ROE、样本数)

sector_summary['avg_pe'] = sector_summary['avg_pe'].round(2)

sector_summary['avg_roe'] = sector_summary['avg_roe'].round(2)

sector_summary = sector_summary.sort_values(['avg_pe','sector']).reset_index(drop=True)

print("\n【板块汇总:平均估值(PE) / 平均ROE / 样本股票数】")

print(sector_summary)

# 6.2 明细结果

res = res.sort_values(['sector','roe'], ascending=[True, False]).reset_index(drop=True)

# 数值字段统一保留两位小数

res['price'] = res['price'].round(2)

res['sector_avg_roe'] = res['sector_avg_roe'].round(2)

res['pe_ratio'] = res['pe_ratio'].round(2)

# roe_5y 是列表,需要单独处理

res['roe_5y'] = res['roe_5y'].apply(lambda lst: [None if v is None else round(v,2) for v in lst])

final_cols = ['code','name','sector','price','roe_5y','sector_avg_roe','pe_ratio']

print("\n【最终结果(ROE前30%样本,按板块+最近一年ROE降序)】")

res[final_cols]

可以看我GitHub上对应项目

https://github.com/JizhiXiang/Quant-Strategy

加入社区!打开量化的大门,首批课程上线啦!

更多推荐

8

8 0

0- 0

已为社区贡献4条内容

已为社区贡献4条内容

所有评论(0)